Wisdom

What a difference a few months make. Last fall I dropped off our toddler Lucy, at preschool, nervous she wouldn’t make it through the first day without melting down. Today, she ended preschool as a young girl, brave, ready to tackle elementary school, and BIG! Look at the difference in the picture.

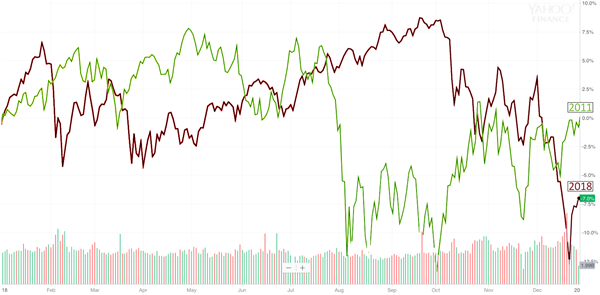

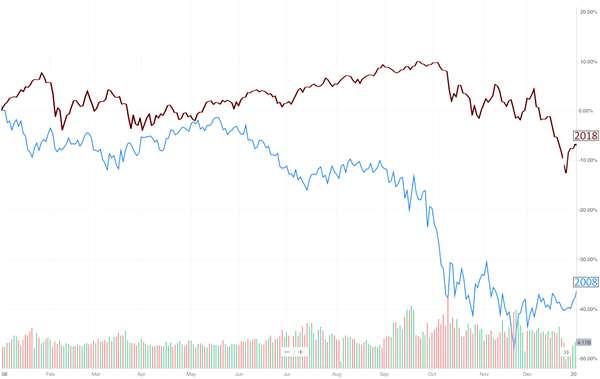

This is also how it’s been with the stock market over the same time period. Last fall we were nervous the trade-war with China would ruin everything! Then, we watched the meltdown at the end of last year followed by an incredible recovery as the nervousness subsided. Now, the market is heading down again for THE VERY SAME REASON!

It reminds me of something I read recently. Tim Keller explained a Proverb and had this to say about Wisdom, “Wisdom invites people to learn from her, but she does not do so from the ivory tower, but outside, in the public square and the public places of the city…Wisdom cannot be conveyed by TED talks or executive briefings….Wisdom comes from experience.”

Armed with her latest experience, Lucy is wiser and will do better in kindergarten next year. In the same way, we are wiser and ready to take advantage of this never-ending cycle of trade drama… and random tweets.

Market News

Every month so far this year has seen positive returns, until May. With today’s tweet about new tariffs on Mexico, the market is now down over 6% for the month. Fair warning for your next statement! Year-to-date, however, the stock market is still positive approximately 10.7%.

From our perspective, the main reason the market’s down is because of a failed effort to close a trade deal with China and now rising concerns about other tariff threats on countries closer to home. Other than trade, the economy still appears to be doing ok.

Unemployment is incredibly low at 3.6% nationally, 4.3% in OR ( ranked #40), and 4.7% in WA (ranked #45). Earnings of companies in Q1 were better than expected, down only slightly at -0.4% and expected to return to growth by Q3, and housing in Portland is still holding up with a 3% increase in prices from one year ago, but slight declines in prices over the last 2 months.

Portfolio Adjustments

The good news is we sold a few investments that had gains as the market started to get volatile earlier in the month. For people in the Moderate Funds portfolio, we sold First Trust Technology Fund FDN. That fund had a significant gain in the 6 months we owned it and we reinvested that money in short-term bonds.

For the Growth Stock portfolio, we sold 3 stocks: Hasbro HAS, IQVIA Holding IQV, and Facebook FB. We sold these to take some profits, but also to raise cash to be able to reinvest if the market continues to pull back.

The stock market is now down enough where we’re interested in beginning to buy again. Just today I added a small amount to computer chip maker Nvidia NVDA in the Growth portfolio. Also, we’re getting ready to buy Microsoft MSFT as a replacement for Facebook if it drops below $120/share. In the Moderate portfolio, we’re considering buying that same fund, First Trust Tech Fund FDN, so we can try to ride it higher once again. We’d like to see it down a little further before we pull the trigger.

Three events were watching over June and July will determine if the stock market heads lower or bounces back up: the G20 summit, Federal Reserve discussions, and Q2 earnings.

The G20 summit is coming up later in June and the meeting there between the US and China will give us an indication if trade talks will resume between the two countries.

After raising rates starting Dec 16, 2015, the Federal Reserve will be meeting this month to determine if it’s time to begin to CUT rates now. Typically, the Fed cuts rates to spur growth when they see a slowing economy. The general consensus is that they will cut rates at least once this year.

Finally, Q2 earnings reporting will begin in July and that will give us an indication if companies are seeing trouble ahead from tariffs or the rest of the world, which are struggling to grow their economies considerably more than the U.S.

No need to worry if the pullback continues. We have cash available in every portfolio and have our shopping list ready to buy as the market gives us opportunities. Our plan is to buy when the market is approximately 10% down from its top, again at 15% down, and then at 20% down. It worked out well at the end of last year and we’ll look to do the same this year.

I apologize for the long letter! We’ll try and shorten it up and have a few more stories next month:)

SMB News

Another quick reminder, in June some of us will be out. I (Tim) will be doing my 3 weeks (usually only 2 weeks) at the Coast Guard, so I’ll be out most the month, but available by email and back in the office in July. Regardless, we’ll make sure there’s someone in to catch the phones and to handle any issues that come up. Please let us know if we can do anything for you and enjoy the nice weather!

– Bruce Porter & Tim Porter, CFP®

Disclosure: Information on this website is for educational purposes only and not intended as investment planning or advice. There is a risk in investing. Account values can go down and the principal can be lost. Not every investment is appropriate for every investor. Any guarantees mentioned are offered by specific financial institutions and not SMB Financial. Some of the information may be out of date. Please consult your own financial advisor or SMB Financial before acting on any of the information. SMB Financial is affiliated with SMB Financial Services, Inc, a registered investment advisor registered with the SEC. The advisor may not transact business in states where it is not registered, excluded or exempted from registration. Individualized responses to persons that involve either the effecting of transaction in securities or the rendering of personalized investment advice for compensation, will not be made without registration or exemption.

can be. Just a change in mood has been enough to erase most the gains in our growth portfolio this year.

can be. Just a change in mood has been enough to erase most the gains in our growth portfolio this year.