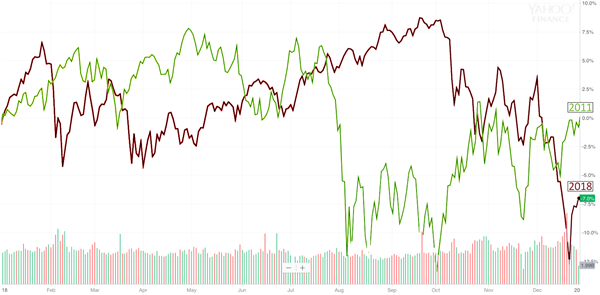

It’s nice to see the sun shine again, on us and especially on the accounts last month. The stock markets are now at their previous highs as fears of a sudden slowdown appear to be in the rearview mirror, but a few concerns still remain.

This afternoon Fed Chairman Jerome Powell stated he was unwilling to cut interest rates at this time. That didn’t help the stock market today because so many were hoping for a rate cut. China trade concerns still linger, but now there’s a report of a deal coming by next Friday. That would be welcome news. Finally, there are concerns related to the 2020 election.

With Biden now officially running there’s no shortage of news of the 20 Democrats campaigning to knock Trump out of the Whitehouse. ONLY eighteen months to go!!! In years past, we’ve downplayed the presidential election as not representing a great impact on the economy or the stock market, but this time feels different.

An example of this is the talk about Healthcare, and specifically the “Medicare for All” position being proposed among several of the Democratic candidates. This has hammered some of the healthcare stocks we own while the general stock market has trended higher.

One of our favorite analysts, Matthew Coffina, CFA from Morningstar, had this to say about the Medicare for All issue, “There are good arguments on both sides of the debate as to whether the U.S. would be better off with a single-payer system. However, as an investor, I’m less interested in what should happen in theory than in what is likely to happen in practice. While Medicare for All would be a potentially catastrophic outcome for private health insurers like Anthem, I still think it’s a very low-probability risk.”

He goes on to say that the biggest impediment to Medicare for All is the cost, citing one “conservative” estimate at $32 Trillion over the next 10 years. To fund that would require doubling the personal income and payroll taxes. While employers would get to eliminate the cost of health care, it’s unclear if the savings would flow to paychecks of employees to help offset higher taxes.

He also mentions that Medicare rates are far below commercial rates and that would bring insurers, hospitals, doctors, pharmaceuticals, etc., out of the woodwork to spend heavily on advertising and lobbying against Medicare for All.

Those powerful interests would be joined by the entire Republican party, which has little incentive to support this type of change. So, Medicare for All probably doesn’t stand a chance unless Democrats win the Presidency, choose a far left candidate like Bernie Sanders in the primary, change the filibuster rules in the Senate, and convince a decent number of moderate Democrats from conservative-leaning states to pass a Medicare for All bill.

Not impossible, but improbable.

In any event, this speculation has been the reason some of the healthcare stocks we all own in our stock portfolio (United Health UNH and Anthem ANTM) have dipped. We actually think this selloff is a great opportunity to buy and will buy more in all accounts if they continue to fall.

SMB News

We’ll all be around the office for the month of May, but starting in June some of us will be out. I (Tim) will be doing my 3 weeks (usually only 2 weeks) at the Coast Guard, so I’ll be out most the month, but available by email and back in the office in July. Regardless, we’ll make sure there’s someone in to catch the phones and to handle any issues that come up. Please let us know if we can do anything for you and enjoy the nice weather!

– Bruce Porter & Tim Porter, CFP®

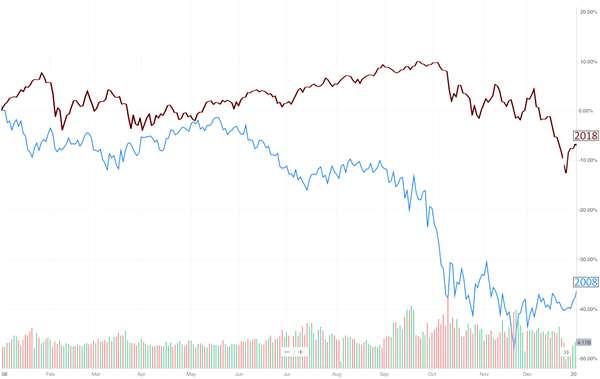

can be. Just a change in mood has been enough to erase most the gains in our growth portfolio this year.

can be. Just a change in mood has been enough to erase most the gains in our growth portfolio this year.